Accidents can happen, even for the most cautious riders. Every year, cyclists in the U.S. experience nearly a half-million bicycle-related injuries, causing damage to both bodies and bikes — as well as sometimes damaging the property of others.

Thankfully, most bicycle mishaps aren’t fatal — or even serious — but every cyclist is reminded of the risks of injury or bike damage every time they ride.

It doesn’t take much to create a cycling disaster. A distracted driver or a surprise obstacle around a blind corner can spell instant trouble — and cyclists are particularly vulnerable.

Jump to Best Insurance Providers

Until recently, the insurance options for U.S. cyclists have been a less-than-perfect solution made of cobbled-together compromises and unsettling gaps in coverage.

Until recently, the insurance options for U.S. cyclists have been a less-than-perfect solution made of cobbled-together compromises and unsettling gaps in coverage.

Some forward-thinking companies are changing all that by providing insurance specifically designed for cyclists, ranging from coverage for bikes and medical needs to preferred-rate life insurance policies.

Am I covered?

Bike theft is also on the rise, with an estimated 1.5 million bicycles stolen in the U.S. each year, only a small percentage of which are ever recovered.

Taking cues from established markets in the U.K., Australia, and other European cycling havens, American insurers are bringing insurance customized for the needs of cyclists to the U.S., answering the nagging question: “Am I covered?”

Contents

Insurance for Bikes and More…

The trouble with bicycle insurance in the past — and insurance for cyclists — is that there hasn’t been a complete solution.

First, let’s look at the usual options — and why they might not be a perfect solution for today’s higher-cost bicycles.

The Bike: Coverage for Theft or Damage

Depending on the reason for the insurance claim, the bike itself might be partly covered under a home insurance policy or a renters insurance policy — but there are some issues with this approach.

Depending on the reason for the insurance claim, the bike itself might be partly covered under a home insurance policy or a renters insurance policy — but there are some issues with this approach.

- Home insurance policies usually have a high deductible. If you’re familiar with insurance, you’ll know the deductible is the part of the claim you pay. Most home insurance policies have deductibles ranging from $500 to $2,500 — or higher.

- Chances are good that your personal property (including the bike) aren’t covered for the full cost of replacement. Most home insurance policies cover your personal property at a depreciated value based on age unless you pay extra to have full coverage for a specific item. For a five-year-old bike that’s damaged or stolen, cyclists can’t expect much in a home insurance claim— if anything at all — after the deductible.

- Crashes may not be covered. Most home insurance policies cover a very specific set of risks. These are called covered perils on your policy. It’s safe to assume that damage due to a risk not named in the policy isn’t covered.

- Mishaps due to racing won’t be covered.

- A home insurance claim is likely to raise rates at renewal or cause you to lose any claims-free discounts you may have. More than one claim in a short period of time can cause your home insurance policy to be non-renewed. Shopping for a new home insurer with claims on your history will be a pricey experience.

Related: Best GPS Trackers For Bikes

The Cyclist: Medical Coverage

Medical coverage for cyclists isn’t as fraught with peril as personal property damage for the bike. If you’re involved in a bike accident and you have health insurance, the injury is handled in the same way as a non-cycling injury.

Medical coverage for cyclists isn’t as fraught with peril as personal property damage for the bike. If you’re involved in a bike accident and you have health insurance, the injury is handled in the same way as a non-cycling injury.

Where home insurance is burdened by coverage exclusions that leave coverage gaps, health insurance exclusions are usually limited to elective procedures or optional care.

One difference in coverage is apparent when an automobile is involved. If you’re injured by an automobile, it’s likely that your auto policy will govern how your medical expenses are paid, often through Med Pay, Personal Injury Protection (PIP), or a combination of both. Once your coverage limits on your auto policy are exceeded, then your health insurance coverage takes over.

Cyclists still need to be mindful of deductibles. The auto-insurance-first structure of medical coverage for auto-related injuries creates a risk of double deductibles if you have a low coverage amount for your auto policy.

If you have a high health insurance deductible or have been thinking about switching, shopping for health insurance has become much easier than in the past.

The Cyclist: Liability Coverage

Liability for cyclists can come in the form of damage to the property of others or bodily injury to others.

Liability for cyclists can come in the form of damage to the property of others or bodily injury to others.

Simply put, a riding mishap can hurt someone else physically — or cause damage to their belongings, including cars, other bikes, signs, or anything else you might bump into with your bike.

Most home insurance or renters insurance policies come with at least $100,000 in coverage for personal liability, and in most cases, the coverage includes payment for legal defense expenses as well. This sounds good, but it’s less than perfect. The primary concern with relying on home insurance for liability coverage is similar to one of the issues with using home insurance for personal property coverage (the bike): Home insurance claims are bad for rates.

Additionally, if you have repeated claims for miscellaneous biking mishaps, you can expect to be shopping for a new home insurance company — if you can find one that will insure you.

What service providers to choose?

Let’s find out…

Velosurance: An Bicycle Insurance Policy Designed for Cyclists (Review)

![]() In 2012, Velosurance partnered with Markel, an international specialty insurer, to provide coverage designed for cyclists, including coverage for electric bikes (up to 750 watts).

In 2012, Velosurance partnered with Markel, an international specialty insurer, to provide coverage designed for cyclists, including coverage for electric bikes (up to 750 watts).

Because the needs of cyclists differ, you can build a customized policy that provides only the coverage you need, without paying for any extras you don’t need.

As a bonus, coverages for your bike that aren’t available through your auto or home policy can be added to your bicycle policy.

When you request a quote, your quote request is reviewed by coverage experts, cyclists themselves, who may suggest changes to your coverage — including removing coverages that are already provided by your auto policy or another policy. In the end, you’re the customer and can purchase the coverage you choose.

Yes, racing is covered, even if you’re a pro.

How It Works

Velosurance is simply trying to save you money if it’s possible that you’ve duplicated coverage. Medical coverage for vehicle contact is a great example because this coverage exists on a standard auto insurance policy. If you have an auto policy, why pay for the same coverage twice?

Dave Williams, CEO and co-founder of Velosurance, estimates the cost of a basic policy to be about 7 to 8 percent of the value of the bike. So, a $3,000 bike can be insured for about $200 per year against physical damage and theft. Coverage options begin at $100 annually.

Because coverage is offered à la carte, rates can vary depending on chosen coverages — but can also vary by location.

Some areas of the country are forced indoors for parts of the year by cold weather, including ice and snow. More use equals more exposure to risk, so cyclists in an area that has great weather year-round can pay more than cyclists in areas where the riding season is limited to 7 or 8 months.

Velosurance’s coverage is good in Canada as well — with no extra charge, but you’ll have to forgo roadside assistance when cycling in The Great White North. Worldwide coverage is available as an add-on for an estimated 10 percent increase in premium.

How Does Velosurance Bike Insurance Work?

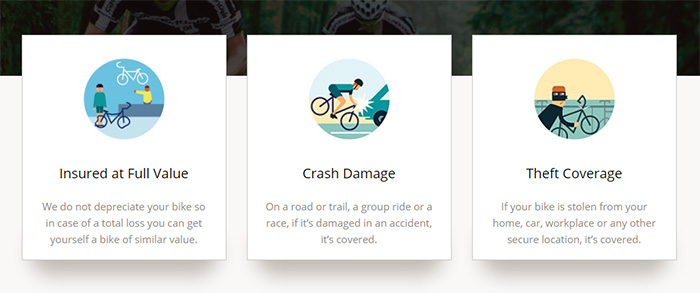

A basic policy for the bike covers any type of sudden and accidental physical loss, including damage or theft. Wear items, like tires and brake pads, aren’t covered.

Unlike auto insurance, which — with the exception of collector-car insurance — depreciates the value of the vehicle and lowers the coverage amount over time, Velosurance provides full replacement cost coverage.

Roadside assistance and access to a nationwide bike shop partner network are among the other extra goodies available through Velosurance.

Your coverage amount is for the stated value of the bike. Be sure to include any add-ons or upgrades you’ve bolted on to your ride. If you buy a new bike for $4,000 and insure it for $4,000, 5 years later, you bike is still insured for $4,000.

Bicycle clothing, however, is paid based on a depreciated value in a covered claim. Fair enough, clothing is used merchandise with only a fraction of the bike’s value.

Much like auto insurance, bike insurance through Velosurance is limited to personal use only. The risks for recreational fitness riders differ from those for a bicycle messenger service weaving through city traffic.

Deductibles — your out-of-pocket costs — range from $100 to $500 with a $300 deductible option providing an attractive balance between affordable premiums and reasonable out-of-pocket costs.

Velosurance’s bike policy is a permissive use policy, which means it provides coverage even if you lend your bike to a friend — including liability and medical coverage if you’ve chosen those coverages for your policy.

Good to Know:

- Yes, racing is covered, even if you’re a pro.

- Trusted partner shops nationwide can provide repair estimates if your bike is damaged.

- Most claims are settled within 14 days.

- We believe it’s the best bike insurance.

Velosurance Optional Coverages

Basic coverage for the bike itself is the policy choice with the lowest premiums, but Velosurance also provides some policy options to help fill potential gaps in coverage:

- Worldwide Coverage

- Medical Coverage — can be used to supplement your existing health coverage

- Vehicle Contact Protection — for those without an auto insurance policy

- Personal Liability Coverage — helps keep your home insurance policy claims-free

With the ability to choose your own coverage limits and options, your policy is as affordable as you need it to be. Quotes are free, with no obligation.

Final Thoughts

It isn’t uncommon for cyclists to invest several thousand dollars in their bikes, and often over $10,000. It can all be gone in an instant due to theft or an accident.

Relying on home insurance or renters insurance can provide some protection — but frequently only a fraction of the loss — and the risk of higher rates when placing a home insurance claim is enough to make any cyclist think twice about even using the coverage.

Velosurance answers those nagging coverage questions and provides a policy cyclist can count on.

Similarly, HealthIQ is shaking up things in the life insurance industry by rewriting the rules for underwriting. Measurable health benefits associated with cycling earn the preferred rates deserved though this forward-thinking agency.

Cyclists in good health can buy enough coverage to protect the family at a price that still leaves plenty of room in the budget for bike gear.

These two companies are taking impressive strides when it comes to insurance for cyclists. In the coming years, we expect even more companies to rise to the challenge and provide innovative insurance solutions for the cycling community.

Message sponsored by Velo Insurance. Do your own research too. There are several bike insurance companies out there.

Hi Phillip,

But of course! They will be convered in future articles and updates. But we feel there is nothing wrong with Veloinsurance. 😉

Can you help me understand how theft works? If I insure my ebike and it ends up stolen, will velo reimburse me the value of the bike covered by the policy? Thank you.

Hi Ernest,

I am sorry to hear about your bike. Have you read this link about bike theft? Velo Insurance

Can u expand on that. Have been considering them for a while

DO NOT BUY VELOSURANCE. In paper they look good but they will do anything on their power to avoid paying.

Hi Carlos,

Any additional information? Let me know on [email protected]

My bike is $500 is there a no deductible plan?

Hi Daniel, I really cannot answer that question. It depends on a lot of factors.